Joe Phelon - Discussed sign ordinance. Requests approval to place temporary signs in public areas to let residents know where and when caucus meetings will be held. Shouldn't be viewed as political if it is open to all political parties. Signs would be removed day after caucus. This is allowed by city code and will be allowed.

City Reports

CM Rees - Members of the Parks and Trails Committee have met with someone in the city who is interested in redoing the roundabout on Cedar Hills Drive as part of an Eagle Scout project. Staff has expressed some concerns with the project because of the number of utility lines going through the roundabout and the issues that surround making significant changes. We will discuss in our meeting this week and I will report back to the Council. Family Festival Committee continues to work on Family Festival.

David Bunker - ULCT semi-annual training in St. George is the first week of April. Rec department will be adding pickleball and a soccer tournament to the Family Festival. Easter Egg hunt is coming up. Golf course is open. Emergency Mgmt meeting was a huge success with over 300 attendees.

Mayor Gygi - Finance Committee met and items discussed will be discussed during budget session in Council meeting. LPPSD met and is dealing with employment issues.

CM Geddes - Utah Valley Dispatch met but he was unable to attend. No big issues discussed.

Consent Agenda

Minutes from the February 16, 2016 City Council meeting were approved.

Discussion on FY 2017 Water & Sewer Fund and Excise Tax Debt Service Fund

Bowen, Collins, and Assoc (BCA) was asked to look at how the city could finance PI meters if the city decided to go in that direction. BCA looked at several options and provided the city with four alternatives. The following comes directly from the BCA report:

Alternative One - No PI Meters

Our understanding is that the City has not made any final decisions with regards to installing PI meters in the City. For comparison purposes, the option to maintain the PI system without metering secondary use is included in this analysis.

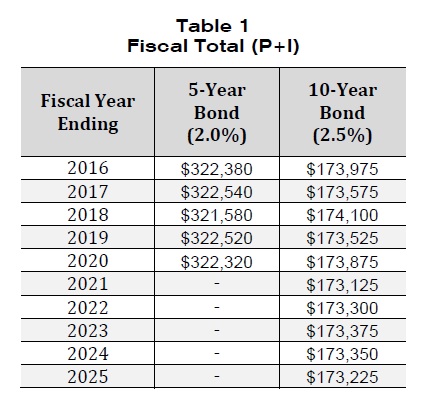

Alternative Two - Install PI Meters Immediately, Pay with 5-year Bond

The City could reasonably plan for the design and installation of PI meters City-wide within the next calendar year and finance the project with a 5-year bond. This alternative uses a preliminary 5-year

amortization schedule provided to the City by Lewis Young Robertson & Burningham (LYRB). Debt service payments would begin in either fiscal year ending (FYE) 2016 or 2017 and last for 5 years.

Alternative Three - Install PI Meters Immediately, Pay with 10-year Bond

The City could also potentially finance the project with a 10-year bond. This alternative uses a preliminary 10-year amortization schedule provided to the City by LYRB. Debt service payments would begin in either fiscal year ending (FYE) 2016 or 2017 and last for 10 years.

Alternative Four - Install PI Meters in Future, Pay with Cash Reserves

The final alternative would not require the City to take on any more debt, but would delay the timeline of the project substantially. Because current revenues from pressurized irrigation rates exceed the costs of paying for the PI system (including O&M, existing debt service, and other capital improvements), the City could deposit the excess revenues into reserves and pay cash for the $1.5 million metering project at some point in the future. While estimates will vary somewhat based on water needs, other capital improvements, growth (or lack thereof) within the City, and the current balance of cash on hand, BC&A has determined that this alternative would push the implementation of the PI metering project into the future approximately 10 years1 (FYE 2025) using the updated PI rate model.

The financing for options 1 and 2 would look like this:

BCA believes that installing PI meters would result in a savings in capital improvements and O&M. Again from their report:

Aside from smaller miscellaneous PI projects that would be required, the City anticipates the need for repair and replacement of several irrigation pumps over the planning window. Due to the additional wear and tear on the PI system from overconsumption, it has been assumed that approximately $300,000 of capital improvements would be required approximately every 5 years, beginning in FYE 2019 if meters are delayed or not installed. If PI meters are installed, capital costs for irrigation pump replacement will decrease substantially. It has been assumed that once PI meters are installed, approximately $150,000 (one half of $300,000) of capital improvements would be required approximately every 10 years, also beginning in FYE 2019.

There are also likely to be significant O&M savings that must be considered in the case that PI meters are installed. BC&A has estimated that approximately $70,000 in utility costs can be saved per year once PI meters are installed, due to decreased pumping demand in the system3. Over the estimated 20-year life cycle of the PI meters, these annual savings will total approximately $1.4 million.

Considering only the costs discussed in this memorandum, the net costs of each alternative are as follows:

- Alternative 1 - $1.2 million

- Alternative 2 – $581,340

- Alternative 3 – $705,425

- Alternative 4 - $1.6 million

In the short term, Alternatives 1 and 4 have less of an impact on the City’s cash flow into and out of the water fund. As expected, implementing PI meters immediately (Alternatives 2 and 3) will have an impact on the City’s short term cash flow, but due to O&M savings over time, have a net cost lower than the other alternatives.4 From a financial perspective, Alternative 2 is the most attractive option over the long term, and by about FYE 2030 is the least expensive option.

The entire BCA memo from January 2016 can be found on my Council blog here.

Questions I would like staff to research:

- The State has indicated they may mandate water metering and recognize they would need to help pay for this. I'd like to hear from ULCT as to what they think is happening with this. Mayor Gygi said he has talked with some legislators and ULCT and the Governor's office seems anxious to move forward but legislators are non-committal.

- Some residents have expressed they feel that we would not see a reduction in usage now that residents receive an electronic statement and can auto pay. Some feel that people will just let the bill pay process be automatic and not reduce usage as they aren't paying attention to changes in monthly bills. I'd like to know what other cities who have implemented PI metering are seeing as far as reduction and if they handle utility bills the same way we do.

- I would like to see the study done by BCA where they determined savings realized by other cities to determine if we are doing an apples to apples comparison. I recognize this may be something we have to do, but it's going to be an unpopular decision and I want to be confident that anything we do is going to fix the issue we are trying to fix. I know many residents are frustrated feeling that the city bonded for PI system with the understanding residents could use as much PI water as they wanted at a flat rate. We now realize this isn't feasible; however, we need to make sure any new projects have a high probability of realizing the savings we are expecting.

Highlights for the Water & Sewer Fund for FY 2017:

- $711,032 wages and benefits

- $534,038 Timpanogos Special Service District (Sewer Charges)

- $399,000 principal payments on debt service

- Extra principal payment of $22,000 on 2009 Utility Revenue Bonds

- $225,512 interest and trustee payments on debt service

- 2006 Utility Revenue Bonds refunded with issuance of 2014 Utility Revenue Bonds for a $402,777.04 net present value benefit

- $294,037 Rocky Mountain Power electrical costs

- $202,349 water purchases—Central Utah Water Conservancy District, Pleasant Grove Irrigation Company, American Fork

- $78,856 excise tax bonds debt service allocation (Public Works building)

- $68,376 motor pool charges

- $68,103 storm drain maintenance

- $66,075 professional services for well rehab, utility rate study, and financial software

- $59,140 meter installation and maintenance--Bridgestone

Here is a helpful utility rate comparison with other nearby cities:

One of the reasons our rates are higher than most is because other cities collect much more in impact fees than we do, especially now that we are almost built out, so we are accruing for future O&M needs that won't be paid for with impact fees. Here is a comparison of impact fees collected:

In the 2012 study, gradual rate increases were proposed by BCA from 2013-2018 to cover estimated operating & maintenance costs for rehabilitation or replacement of system components, plus capital improvements, and debt service (pay as you go philosophy):

- Culinary water rates increase 6.4% a year

- Pressurized irrigation (PI) rates remain flat

- Sewer rates increase 5.5% a year

- Storm drain rates increase 6.5% a year

- Total utility increase 3.7%-4.3%

BCA Recommendations:

- Recommended storm rate increases decline from 6.5% to 6.0% 2022-2025

- Recommended sewer rate increases stays at 5.5% through 2025

- Recommended pressurized irrigation rate stays flat through 2025

- Recommended water rate update depends on alternative chosen to deal with water consumption

- Alternative 1—Status quo, no secondary meters and no additional wells

- Water fee increases 6.4% annually through 2025

- Alternative 2—New secondary meters $1.5 million w/five-year bonds at 2%

- $900,000 used from unrestricted net position and $600,000 from bonds

- Water fee increase the same until year 5, then 8.0% decrease

- Costs city approximately $230,000 less than alternative 3 annually

- 33% less demand

- $70,000 in power savings per year

- $45,000 in pump and equipment cost savings per year

- Alternative 3—Additional well and updates to pumps, pipelines $3.5 million

- Water fee increase additional 8.0% first year, and 5.8 % second year, 6.4% each year after that

- Timing Changes

- Old Town retention project moved from FYE 2016 to FYE 2020 $400,000, PG irrigation may change timing and scope

- Canyon road sewer moved from FYE 2014 to FYE 2021 $400,000

- 4000 West sewer moved from FYE 2016 to FYE 2020 $250,000

- 4600 West sewer moved from FYE 2018 to FYE 2020 $400,000*

- *Projects may be adjusted based on timing of road projects

- Migratory meter read project to continue through FYE 2017

- Other projects

- Harvey well chlorination station FYE 2020 $80,000

- Cottonwood well chlorination station FYE 2020 $60,000

- Cedar Hills drive sewer upgrade FYE 2020 $400,000

- Sewer outfall line extension FYE 2021 $500,000**

- **Following the SECAP study, sewer projects timing will be refined

- Additional capital improvements from 2012 study

- New Jet/Vacuum truck for FYE 2018 $300,000

- Storm drain improvements for golf maintenance building for FYE 2016 $100,000

- Irrigation pumps at Pond 10 and 12 will be adjusted, if necessary

- Harvey well replacement FYE 2025

Finance Director is requesting that we separate debt service from capital projects fund. Here are details on the reasons for this, per GASB:

- Capital projects funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays, including the acquisition or construction of capital facilities and other capital assets. Capital projects funds exclude those types of capital-related outflows financed by proprietary funds.

- Debt service funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for principal and interest. Debt service funds should be used to report resources if legally mandated. Financial resources that are being accumulated for principal and interest maturing in future years also should be reported in debt service funds.

- Excise Tax Debt Service Fund

- Move debt service related to Public Works building from the capital projects fund to a debt service fund for budget purposes

- Combine debt service fund with general fund for financial reporting purposes

Staff also provided information on creating a special fund to cover expected litigation costs:

- Alternative for budgeting volatile transactions like litigation and tort claims, which may allow the general fund to have more consistent legal expenses year to year

- Governmental Immunity Special Revenue Fund

- Create a risk insurance fund that funds and tracks litigation and tort claims

- Maximum tax levy rate allowed is .0001 or $42,982 in the current fiscal year

- May require truth-in-taxation, if combined aggregate rate exceeds certified tax rate

- Budget as a special revenue fund to manage and combine with general fund for reporting purposes

- Only increase property taxes if significant litigation expenditures are expected the next fiscal year, and/or current year litigation drains general fund reserves

- Amount allowed for tax under Tort Liability/Governmental Immunity 63G-7-704(2)(c) is 050 0.000100, which for us is equal to $42,982.

Questions I have for research:

- This year the State Legislature made some changes to cities bonding for judgments against cities. I'd like to know how this affects us if we do lose in any litigation and the pros and cons of going in this direction instead of creating this new fund. David Shaw is going to provide the Council with further information on this new law.

We had a joint meeting with three members of the Planning Commission tonight. CM Zappala gave a brief overview of changes that were made to Design Guidelines. Has tried to remove duplicate language also found in city code. Language in introduction and vision are mostly unchanged from original document. Districts have been better identified. Zone for Walmart was updated to Neighborhood Retail as it is a high-intensity use. Use table has been completely updated and is based on use tables from other cities, especially PG and Provo. Still needing feedback from legal on changes that have been made to allowed uses. Residential uses now have very specific guidelines for density and location (ex: only allowed on second floor). Planning Commission a lot of valuable feedback and these suggestions/changes will be incorporated in to the document.

No comments:

Post a Comment